Understanding how inflation impacts retirement savings is one of the most important things any pre-retiree can do. Most retirement plans are built around nominal numbers — account balances, contribution limits, projected growth rates. But none of those figures account for the one force that quietly erodes their value every single year: inflation.

A 2% or 3% annual rise in prices may not feel alarming in the moment. Over a 20-to-30-year retirement, however, that seemingly modest rate compounds into a significant reduction in purchasing power. The groceries, healthcare, utilities, and housing you plan to fund with your savings will cost considerably more in 2040 or 2050 than they do today.

This article walks through exactly how inflation impacts retirement savings, what the numbers look like in practice, and which strategies — including inflation-resistant assets like gold — retirement investors have historically used to preserve their wealth.

⚠️ Important Disclaimer

This article is for educational purposes only and does not constitute financial or investment advice.

Always consult a qualified financial advisor before making investment decisions.

What Is Inflation and How Does It Work?

Inflation is the rate at which the general level of prices for goods and services rises over time — and correspondingly, the rate at which the purchasing power of currency falls. It is measured in the United States by the Consumer Price Index (CPI), published monthly by the Bureau of Labor Statistics.

The Federal Reserve targets a 2% annual inflation rate as a sign of a healthy, growing economy. At that level, inflation is considered manageable. But even at 2%, the cumulative impact over two or three decades is significant. At 3%, it becomes substantial. During periods of elevated inflation — like the post-pandemic surge that saw CPI peak above 9% in mid-2022 — the damage to fixed-income savers can be severe.

The mechanism is simple: when prices rise, each dollar in your retirement account buys less than it did before. This is why inflation impacts retirement savings so directly — the nominal balance in your account doesn’t change, but its real-world value quietly shrinks.

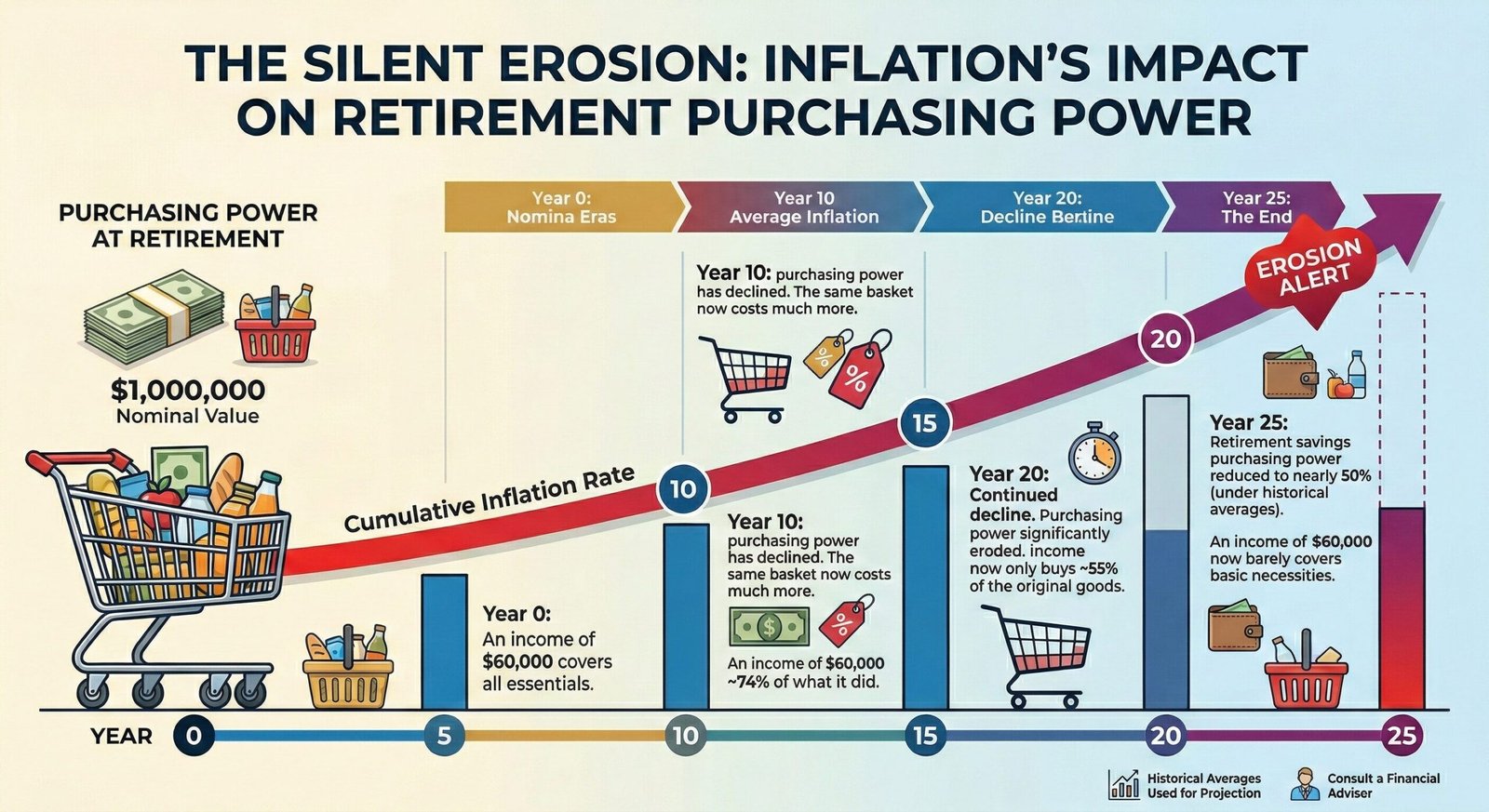

How Inflation Impacts Retirement Savings in Real Numbers

To understand how inflation impacts retirement savings concretely, consider a retirement account with $500,000 today. That balance doesn’t move — but at 3% annual inflation, here is what happens to its purchasing power over time:

| Year | Nominal Balance | Purchasing Lost Power | Real Buying Power |

|---|---|---|---|

| Today | $500,000 | – | $500,000 |

| Year 5 | $500,000 | $68,700 | $431,300 |

| Year 10 | $500,000 | $127,950 | $372,050 |

| Year 15 | $500,000 | $179,100 | $320,900 |

| Year 20 | $500,000 | $223,200 | $276,800 |

| Year 25 | $500,000 | $261,300 | $238,700 |

In plain terms: $500,000 today has the purchasing power of roughly $238,700 twenty-five years from now — at a moderate, historically average inflation rate. The account balance didn’t fall. Inflation impacts retirement savings by silently consuming more than half of what that money can actually buy.

If your portfolio grows at 6% annually while inflation runs at 3%, your real return is approximately 3% — before taxes and fees. This is known as the real rate of return, and it’s the figure that actually determines whether your retirement is funded.

The Categories of Retirement Spending Most Affected by Inflation

Not all expenses inflate equally. When considering how inflation impacts retirement savings, it helps to understand which spending categories typically outpace general CPI:

Healthcare

Medical costs have historically risen faster than general inflation. The Centers for Medicare & Medicaid Services projects U.S. healthcare spending to grow at an average of 5.6% annually through 2031. For retirees who spend significantly on prescriptions, procedures, and insurance premiums, this is one of the most acute areas where inflation impacts retirement savings.

Housing

Property taxes, maintenance costs, and utility bills tend to rise steadily over time. Renters face additional exposure to local rental market conditions, which can spike dramatically in certain regions.

Food and Groceries

Food inflation can be volatile. The 2021-2023 inflation surge demonstrated this clearly, with grocery prices rising well above the headline CPI rate in certain months.

The 4% Rule and Inflation Risk

The widely cited 4% withdrawal rule — which suggests retirees can withdraw 4% of their portfolio annually without running out of money — was developed based on historical market data. However, sustained periods of above-average inflation can erode even a carefully constructed drawdown strategy. This is one reason financial planners increasingly stress the importance of building inflation-resistant components into retirement portfolios.

Why Inflation Impacts Retirement Savings More Than Working Years

During your working years, wages often rise with inflation. You receive a cost-of-living adjustment, earn more in a competitive job market, or simply charge more for your services. This built-in hedge largely disappears in retirement.

In retirement, most people draw on fixed or semi-fixed income: Social Security, pension distributions, and portfolio withdrawals. Social Security does include a Cost-of-Living Adjustment (COLA) — but the SSA’s COLA formula has historically underrepresented the actual inflation experienced by older Americans, particularly in healthcare. This gap is one reason how inflation impacts retirement savings is so much more acute post-retirement than during your accumulation years.

The combination of fixed income, rising expenses, and a longer life expectancy than previous generations creates a compounding vulnerability that every retirement plan should address.

How Inflation Impacts Retirement Savings Held in Different Asset Classes

Not all retirement assets respond the same way to inflation. Understanding how inflation impacts retirement savings across different vehicles helps investors make informed decisions about portfolio composition.

Bonds and Fixed-Income Assets

Traditional bonds are among the most vulnerable assets when inflation rises. The fixed coupon payments that bonds offer become worth less in real terms as prices increase. Long-duration bonds are especially sensitive — a scenario that played out dramatically in 2022 when rising inflation caused bond prices to fall sharply.

Equities

Stocks have historically provided some protection against inflation over the long run, as corporate revenues and earnings can rise with prices. However, during acute inflationary spikes, equity markets can experience significant volatility and short-term losses — precisely when retirees may need to draw down their portfolios.

Gold

Gold has a long historical record as an inflation hedge. While it does not perfectly mirror CPI in any given year, its purchasing power has tended to remain relatively stable over long periods. Our detailed article on gold vs inflation — does it still work? examines this relationship with historical data.

Importantly, gold operates independently of the financial system — its value is not tied to the creditworthiness of any government or corporation. This characteristic makes it particularly relevant when inflation is driven by monetary policy, as was the case during post-2020 quantitative easing programs.

For those approaching or in retirement, a portion of the portfolio in gold can serve as a stabilising counterweight to the inflation risk embedded in bonds and cash holdings. To understand how this fits into a broader framework, see our complete guide to gold investing fundamentals.

Real Estate

Property can serve as an inflation hedge through rising rents and appreciation, but it comes with liquidity risk and management responsibilities that make it impractical for many retirees.

Treasury Inflation-Protected Securities (TIPS)

TIPS are U.S. government bonds specifically designed to protect against inflation — their principal adjusts with CPI. The Treasury Direct resource on TIPS explains how they work in detail. They represent a direct hedge, though their real yields can be low in certain interest rate environments.

Strategies to Protect Retirement Savings from Inflation

Given how significantly inflation impacts retirement savings, building a deliberate inflation strategy is essential. The following approaches are used by retirement investors to preserve purchasing power over time:

1. Diversify Into Inflation-Resistant Assets

No single asset perfectly hedges inflation. A diversified approach might combine TIPS, commodities exposure, real estate investment trusts (REITs), and precious metals. The goal is to hold assets whose real value tends to hold up — or rise — when purchasing power falls.

2. Consider a Gold IRA for Tax-Advantaged Inflation Protection

For retirement investors, a Gold IRA provides a way to hold physical gold within a tax-advantaged retirement account structure. Our guide on Gold IRAs explained in detail covers how these accounts work, IRS eligibility requirements, and contribution limits. Given how inflation impacts retirement savings specifically — not just investments in general — the ability to hold a hard asset inside a retirement account is worth understanding.

3. Monitor Your Real Rate of Return

Most retirement projections use nominal return assumptions. Adjusting for inflation, fees, and taxes gives you the real rate of return — the figure that actually determines how much purchasing power your portfolio will have in 20 or 30 years. Update these projections annually as inflation expectations change.

4. Build Flexibility Into Withdrawal Strategies

Rigid withdrawal schedules can be dangerous in high-inflation environments. Working with a financial advisor to build dynamic withdrawal strategies — including delaying Social Security benefits to maximise COLA-adjusted income — can help extend portfolio longevity.

5. Stay Informed About Macro Trends

Inflation doesn’t exist in isolation. Central bank policy, government spending, and global economic conditions all influence its trajectory. Our analysis of why central banks are buying gold again provides context on how institutional actors are positioning for long-term inflationary risk. And for forward-looking data, our gold price outlook for 2025–2030 provides expert forecasts relevant to retirement planning.

How Much of Your Portfolio Should Be Inflation-Resistant?

There is no universal answer — allocation depends on your age, risk tolerance, existing income streams, and overall financial plan. General guidance from financial planning professionals suggests:

- Ages 55–65 (pre-retirement): Focus on gradually building inflation-resistant exposure as you approach the drawdown phase

- Ages 65–75 (early retirement): Consider 10–20% in hard assets and inflation hedges depending on income stability

- Ages 75+ (late retirement): Prioritise capital preservation and income reliability; gold and TIPS may play a stabilising role

These are general frameworks, not personalised advice. A qualified financial advisor can help you assess how inflation impacts retirement savings in your specific situation.

📘 Further Reading

-> Gold vs Inflation: Does It Still Work?

-> Gold IRAs Explained in Detail

-> Complete Guide to Gold Investing

-> Why Central Banks Are Buying Gold Again?

-> Gold Price Forecast 2025–2030

Conclusion

Inflation impacts retirement savings in ways that are easy to underestimate — especially when you look only at nominal account balances. A $500,000 retirement fund can lose more than $260,000 in real purchasing power over 25 years at a moderate 3% inflation rate, without a single dollar being withdrawn.

The investors best positioned for retirement are those who understand how inflation impacts retirement savings and build their portfolios accordingly: with diversified exposure to inflation-resistant assets, tax-advantaged vehicles, and flexible withdrawal strategies.

Gold has historically served as one component of that inflation defence — not as a speculative bet, but as a long-run store of value that operates outside the monetary system. Whether through direct ownership, a Gold IRA, or gold ETFs, understanding the role precious metals can play is a meaningful step toward a more resilient retirement plan.

For a comprehensive introduction, explore our complete guide to gold investing fundamentals. For retirement-specific strategies, our Gold IRAs explained in detail page is the best starting point.