Deciding on the right gold allocation strategy is one of the most consequential — and most frequently mishandled — decisions in retirement portfolio planning. Get it too low and gold provides little meaningful protection. Get it too high and you have concentrated exposure to a non-income-producing asset that can lag equities for years at a stretch.

The goal, as your Starter Kit puts it, isn’t to predict whether gold will go up or down. It’s to build a portfolio that can handle multiple economic environments without requiring you to guess which one is coming. That is the philosophical foundation of any sound gold allocation strategy: structural resilience, not directional betting.

This guide covers everything you need to determine your own allocation — the standard ranges financial professionals recommend, how life stage affects the calculus, how gold behaves across different economic scenarios, a practical checklist for readiness, and how to implement your gold allocation strategy across different account types.

⚠️ Important Disclaimer

This article is for educational purposes only and does not constitute financial or investment advice.

Consult a qualified financial advisor before making investment decisions.

What a Gold Allocation Strategy Actually Does for a Portfolio

Before settling on a percentage, it helps to understand what a gold allocation strategy is actually designed to accomplish. Gold is not in a portfolio to generate income. It pays no dividends, earns no interest, and produces no cash flow. Its role is structural — not generative.

Specifically, a well-designed gold allocation strategy serves three functions:

- Diversification: Gold’s correlation to equities and bonds is historically low, meaning it tends not to move in lockstep with the rest of a portfolio. When stocks fall, gold does not always fall with them.

- Inflation protection: Over long horizons, gold has historically maintained purchasing power better than currency alone — a particular concern for retirement investors facing 20–30 year drawdown periods.

- Systemic hedge: In periods of financial stress, institutional failure, or currency devaluation, gold holds value independently of the financial system. This characteristic is unlike any paper asset.

Understanding these functions makes it easier to size the allocation correctly. You are not buying gold because you think it will outperform equities next year. You are including it because it behaves differently — and that difference has value across a full market cycle. For broader context, see our complete guide to gold investing.

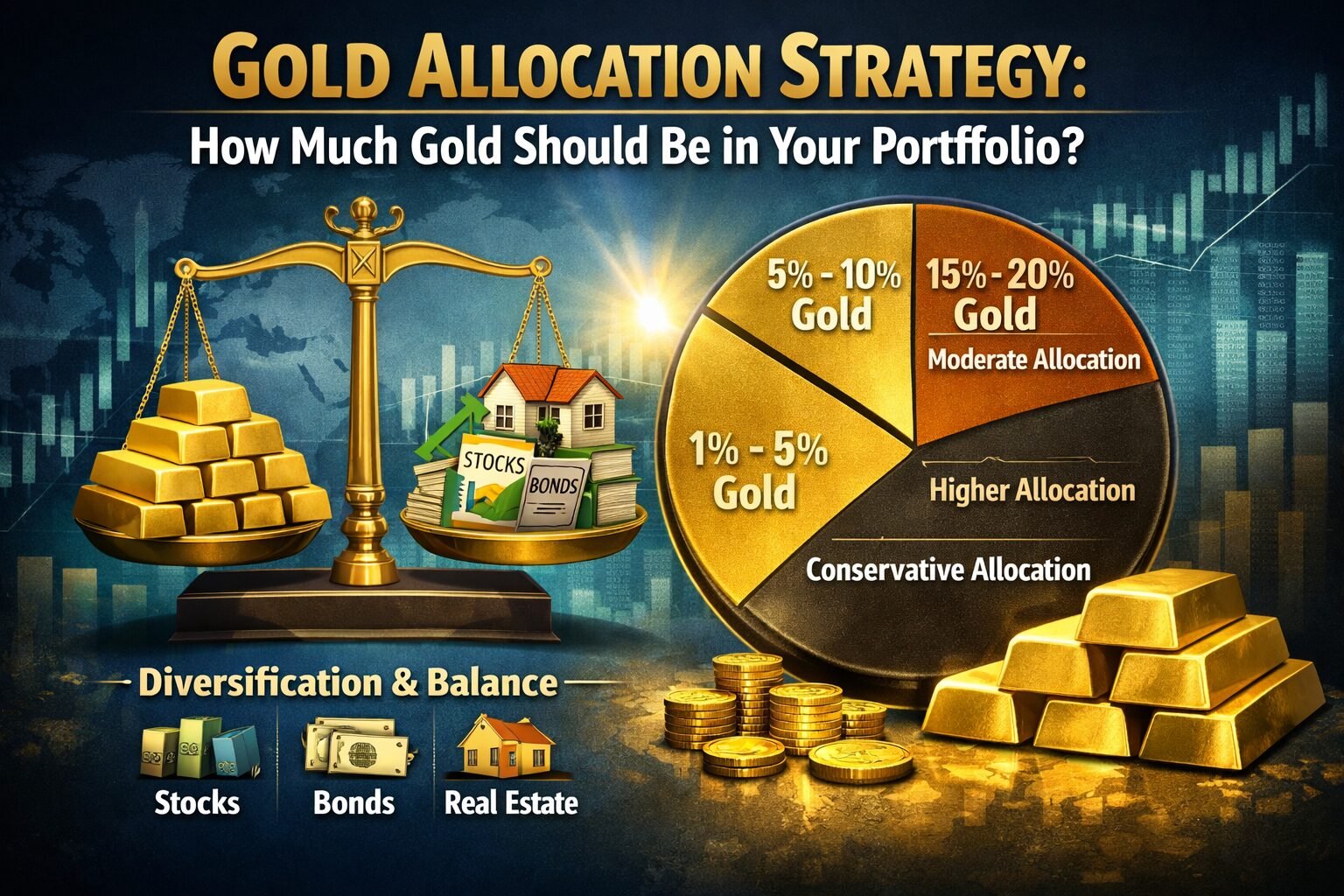

The Standard Range: What Financial Professionals Recommend

The most commonly cited gold allocation strategy range among financial professionals is 5–10% of investable assets. This range appears consistently across independent financial planning literature, academic research on portfolio construction, and practitioner guidance.

The World Gold Council’s research on portfolio construction — one of the most cited bodies of data on gold’s role in portfolios — finds that allocations in the 2–10% range have historically reduced portfolio volatility without materially sacrificing long-run returns. Their modelling suggests the optimal allocation varies with market conditions but tends to cluster in the lower end of this range for most moderate-risk investors.

Why 5–10%? The logic is straightforward: at these levels, a gold position is large enough to provide meaningful diversification and inflation-sensitive exposure, but small enough not to dominate portfolio returns or introduce excessive volatility. Gold’s price can swing significantly in shorter periods — allocating 20% or 30% of a retirement portfolio to gold would create a level of volatility that most retirees cannot absorb.

Beyond 10%, the gold allocation strategy begins to shift from diversification tool to concentration bet. That is the opposite of what prudent portfolio construction requires.

Gold Allocation Strategy by Life Stage

The right gold allocation strategy is not a static number — it shifts across your financial life. The table below outlines general guidance at each stage:

| Life Stage | Gold Range | Primary Goal | Key Consideration |

|---|---|---|---|

| Early Career (25–45) | 2–5% | Growth & accumulation | Equities dominate; gold is a minor hedge |

| Mid-Career (45–55) | 5–8% | Balanced growth & preservation | Begin increasing as retirement nears |

| Pre-Retirement (55–65) | 8–12% | Capital preservation | Reduce equity concentration; gold more central |

| Early Retirement (65–75) | 10–15% | Income stability & inflation hedge | Focus on purchasing power over 20+ years |

| Late Retirement (75+) | 5–10% | Wealth preservation & legacy | Simplify; prioritise liquidity alongside gold |

The key principle is that gold’s role in a gold allocation strategy typically expands as time horizon shortens and capital preservation becomes more important than growth. A 35-year-old with 30 years of runway can ride out equity volatility. A 62-year-old approaching retirement cannot afford the same drawdown tolerance — and a gold allocation provides a meaningful stabiliser.

How Gold Performs Across Different Economic Environments

One of the strongest arguments for a permanent gold allocation strategy — rather than a tactical one — is that gold has historically contributed positively across multiple types of economic stress, not just one. Understanding this helps investors maintain their allocation with conviction through periods when gold appears to lag.

| Economic Scenario | Gold’s Typical Role | Why Allocation Matters |

|---|---|---|

| High Inflation | Strong performer | Preserves purchasing power when currency loses value — core reason for allocation |

| Recession / Equity Bear Market | Typically resilient | Low correlation to equities means gold can hold or rise when stocks fall |

| Financial / Banking Crisis | Strong safe-haven demand | Physical gold independent of counterparty risk becomes especially valued |

| Currency Devaluation | Strong performer | Gold is priced in USD globally; as dollar weakens, gold typically rises |

| Strong Equity Bull Market | Can lag significantly | Growth assets outperform; gold’s value lies in what it does when they don’t |

| Deflation / Low Inflation | Mixed results | Gold may underperform without inflationary pressure; smaller allocation appropriate |

The most important row in that table is the last two: gold can lag in extended bull markets, and it performs modestly in deflationary environments. This is precisely why a gold allocation strategy should be sized at 5–15%, not 30% or 50%. You want the benefits of multiple economic scenarios, not a concentrated bet on one. For data on gold’s historical inflation track record, see our article on gold vs inflation — does it still work?.

How to Implement a Gold Allocation Strategy

Once you have determined your target allocation, the next step is implementation. A gold allocation strategy can be executed through several different vehicles depending on account type, time horizon, and preferences around ownership structure.

Option 1: Gold ETFs in a Standard IRA or Brokerage Account

Gold ETFs such as GLD or IAU can be purchased through any major brokerage and held inside a standard IRA. This is the simplest implementation path — no special account setup required, immediate liquidity, and low transaction costs. The trade-off is indirect ownership through a fund structure rather than the metal itself. For a full comparison, see our guide on physical gold vs gold ETFs.

Option 2: Physical Gold in a Self-Directed Gold IRA

For retirement investors who want direct metal ownership within a tax-advantaged structure, a self-directed Gold IRA provides physical gold exposure inside an IRA wrapper. This combines the counterparty-risk-free characteristics of physical gold with the tax benefits of a retirement account. Our guide on Gold IRAs explained in detail covers the full mechanics, IRS requirements, storage rules, and fee structures.

Option 3: Physical Bullion Outside a Retirement Account

Some investors prefer to hold physical gold coins or bars independently of their retirement accounts — as a direct ownership position outside the financial system entirely. For guidance on reputable dealers and pricing, see our article on where to buy gold bars in 2026.

Option 4: A Hybrid Approach

Many experienced investors implement a gold allocation strategy that combines elements of each: ETFs for liquidity and tactical flexibility inside a standard account, a Gold IRA for the retirement-focused physical component, and potentially a small physical holding outside the financial system entirely. The proportional split depends on individual preferences for ownership structure, tax efficiency, and liquidity needs.

Gold Allocation Readiness Checklist

Before implementing a gold allocation strategy, confirm the following foundations are in place. Gold performs its portfolio role best as a deliberate strategic allocation — not a reactive one made under financial pressure:

- High-interest debt is managed or eliminated

- Emergency fund covers 3–6 months of living expenses

- Core retirement portfolio is diversified across stocks, bonds, and cash

- You understand the inflation risk facing your savings over a 20–30 year retirement horizon

- You have reviewed the differences between physical gold and paper-based exposure

- You are comfortable with a 5–12% allocation that will fluctuate in value year to year

- You have considered storage, tax implications, and a long-term exit strategy

- You are not planning to use this allocation for near-term liquidity needs

If most of these apply, you are well-positioned to implement a gold allocation strategy with clarity. If several do not yet apply, it may be worth addressing those foundations first before adding gold to the portfolio.

Maintaining and Rebalancing Your Gold Allocation Over Time

A gold allocation strategy is not a set-and-forget decision. Gold prices can move significantly in relatively short periods — a strong gold bull market can push a 10% allocation to 15% or 18% of total portfolio value, creating unintended concentration. A rebalancing discipline prevents this.

Most financial planners recommend reviewing asset allocation annually, or whenever any single position drifts more than 5 percentage points above its target. When gold outperforms and grows beyond your target weight, trimming back to target locks in gains and maintains the diversification function the allocation was designed to provide. When gold underperforms and falls below target, rebalancing by adding represents disciplined buying at lower prices.

The rebalancing process also intersects with tax planning — particularly for gold held in taxable accounts, where gains may be subject to the 28% collectibles rate. A Gold IRA eliminates this concern for the portion of your gold allocation strategy held within the tax-advantaged structure. For context on how central banks and institutional investors approach their gold positions over time, our analysis of why central banks are buying gold again offers useful perspective.

Common Gold Allocation Mistakes to Avoid

Over-Allocating Based on Short-Term Price Momentum

The most common mistake investors make with a gold allocation strategy is sizing the position based on recent performance. Gold hitting record highs is not, in itself, a reason to hold 30% of a portfolio in it. Allocation should be driven by portfolio function and risk management principles — not price charts.

Treating Gold as an Income-Generating Asset

Gold does not produce income. It does not pay dividends or interest. An investor who needs their portfolio to generate regular cash flow cannot rely on gold for that function. Gold’s role is capital preservation and diversification — income must come from other portfolio components.

Confusing Exposure for Ownership

An investor who holds gold ETFs believes they have exposure to gold — and they do, in price terms. But they do not own gold. The distinction matters in extreme scenarios. A complete gold allocation strategy for a retirement-focused investor should include some element of direct physical ownership, not solely paper exposure.

Neglecting the IRA Structure

Many investors build gold positions in taxable brokerage accounts without considering the tax advantages available through a Gold IRA. Given the 28% collectibles rate that applies to gold gains in taxable accounts, the tax efficiency of a Gold IRA structure is often significant over a multi-decade holding period.

Conclusion

A sound gold allocation strategy is not about timing the gold market or making a directional bet on prices. It is about building a portfolio resilient enough to handle multiple economic environments — inflation, recession, financial stress, and currency uncertainty — without requiring you to predict which one arrives next.

The 5–10% standard range is a starting point, not a ceiling. Pre-retirees and retirees with longer-term capital preservation priorities may find allocations toward the upper end of the range — or modestly beyond — appropriate for their situation. Life stage, income certainty, and overall portfolio composition all influence the right number for each individual investor.

What matters most is that the allocation is intentional, properly sized, held in the right account structure, and reviewed regularly as circumstances change. That is what a genuine gold allocation strategy looks like — not a speculative overweight, and not an afterthought, but a deliberate structural component of a retirement portfolio built to last. To explore implementation options, visit our guide on Gold IRAs explained in detail. For the full context of gold’s role in a portfolio, see our complete guide to gold investing.